“We must divorce the three golden balls

from the three Furies.”

— Charities Review, 1892

{kind=link}

Installment plans, home mortgages, and auto loans offered new opportunities for people in industrializing societies to get themselves into debt. At the same time, waged employment in booming nineteenth-century cities created a class of borrowers who lacked the social networks necessary for older types of neighborly credit relations and no longer owned the types of productive assets customarily used as collateral.

Together, these developments meant that the ability to incur obligations occasionally outpaced the ability to meet payments, and borrowers could find themselves in financial straits. An industry of secondary credit providers—primarily pawnbrokers and salary lenders—arose to meet the urgent demand for ready cash.

{kind=link}

{kind=link}

{kind=link}

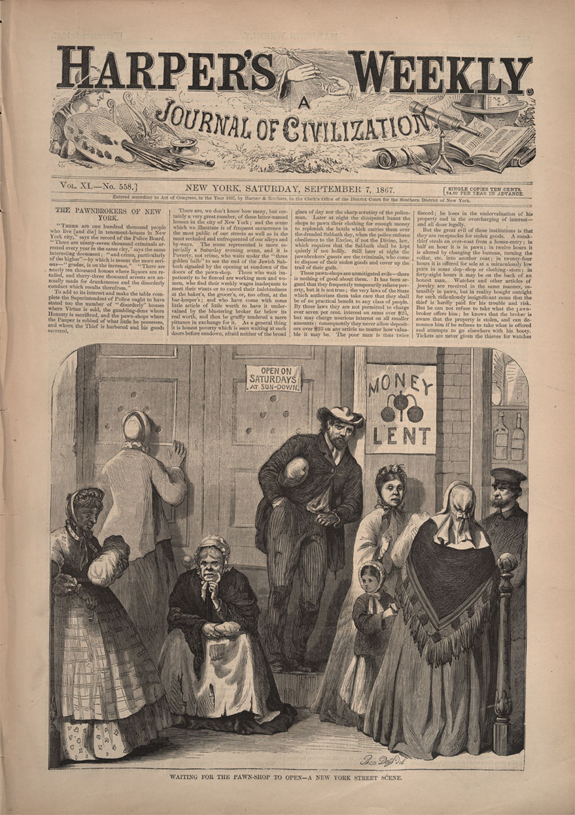

Pawnbroking has changed little since its origins in fifth-century China and medieval Europe: small loans are advanced against personal possessions of the borrower held as collateral. Though they existed in premodern society, pawnshops did not become a ubiquitous presence until the early years of industrial capitalism. Pawnshops were common in eighteenth-century British cities like London and Manchester—the cradle of the industrial revolution—but New York’s first pawnshop was not founded until 1822, and they did not proliferate in American cities until the middle of the next century.25 Pawnbrokers everywhere strove to make themselves instantly recognizable to persons, including illiterate ones, desperate for quick cash. In China, pawnbrokers hung a distinctive decorative staff from their storefronts; in Europe and the United States, the universally recognized symbol was three golden balls.

In twenty-first century China, where the demand for investment capital exceeds the capacity of the nation’s state-controlled financial sector, pawnshops and other informal sources of finance remain an important part of the economy.

{kind=link}

Another type of small lender rose to prominence around the turn of the twentieth century: the salary lender, or “loan shark.” One study of 1894 estimated that one in five American households owed money to one of these lenders. Because the legal lending rate was too high for small loans to be profitable, most “loan sharks” operated illegally, making their customers vulnerable to exploitation.26 The illegality of the industry also poses a challenge for historians. Because most early salary lenders strove to keep their business under the table, historians must piece together the story from criminal investigations and journalistic exposés.

{kind=link}

Attacks on loan sharking in the press also inspired reformers. In 1909, the Russell Sage Foundation, led by the Columbia graduate students Arthur Ham and Clarence Wassam, dedicated itself to “the loan shark campaign” and produced a flood of publications in a variety of media in addition to founding semi-philanthropic financial institutions that offered loans at favorable rates.27 Inspired by Europe’s monti di pietà, charitable pawnshops that offered collateral loans at below-market rates, New York’s leading philanthropists established the Provident Loan Society in the aftermath of the Panic of 1893.28 By 1909, there were fifteen such societies—backed by the likes of Cornelius Vanderbilt and Percy A. Rockefeller—offering small chattel loans on a philanthropic or semi-philanthropic basis. To its borrowers, the Provident Loan Society showed a business face, operating as an ordinary pawnshop. But it boasted interest rates that were one half to one third of the legal rate charged by independent pawnbrokers.29

{kind=link}

{kind=link}

Reformers initially aimed to drive loan sharks out of business. In addition to the program of philanthropic lending, the Russell Sage Foundation pursued an aggressive strategy of prosecutions and publicity against salary lenders.

But they eventually realized that working people could not do without a source of quick cash in times of personal crisis, and their goals changed from extermination to regulation. After 1914, however, a coalition of reformers and lenders cooperated to draft the Uniform Small Loan Law, implemented in twenty-five states by the 1930s. Small lenders moved their offices from dark second-floor apartments, open only evenings and weekends, to brightly lit and well-publicized establishments, and even formed their own industry association and trade publication, the Industrial Lenders News.

The key was a new, higher lending rate. Economists and legislators realized that the bank rate of 6 percent was too low to allow small lenders even a modest profit, and reached a compromise. By 1932, twenty-five states had implemented the Uniform Small Loan Law, legalizing thousands of small lenders and providing some measure of consumer protection for their clients.30

25 William R. Simpson and Florence Simpson, with Charles Samuels, Hockshop (New York: Random House, 1954).

26 Michael Easterly, “Your Job Is Your Credit: Creating a Market for Loans to Salaried Employees in New York City, 1885–1920,” Enterprise & Society 10, no. 4 (2009): 651–660.

27 Malcolm W. Davis, The Loan Shark Campaign (New York: Division of Remedial Loans, Russell Sage Foundation, 1914).

28 James Speyer, “Monts-de-Piété,” Charities Review (February 1895); quote Alfred Bishop Mason, “Things to Do,” Charities Review (March 1892): 212.

29 Rolf Nugent, The Provident Loan Society of New York: An Account of the Largest Remedial Loan Society (New York: Russell Sage Foundation, 1932), 51.

30 Calder, Financing the American Dream, 134.