“A river of red ink runs through American history.”

— Lendol Calder, Financing the American Dream (2000)

{kind=link}

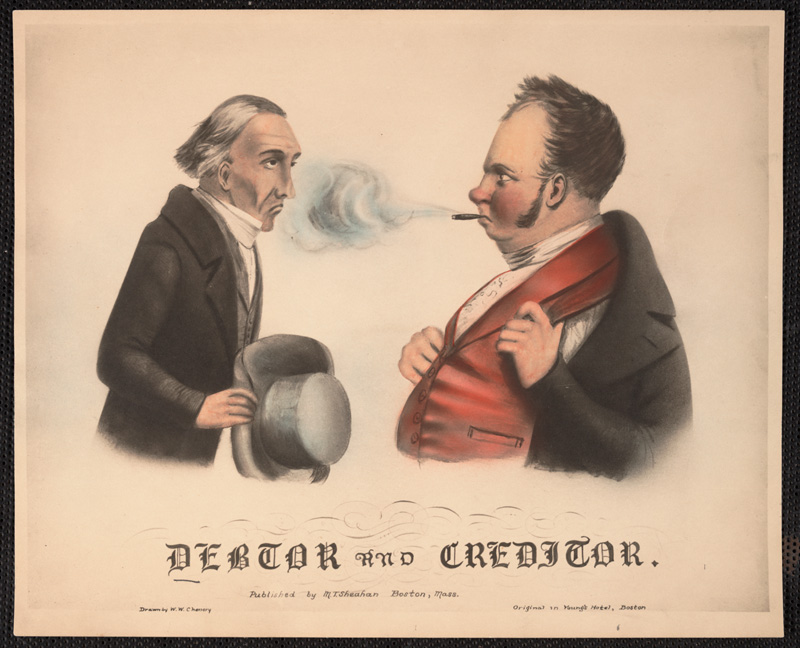

There is a myth of a lost golden age of economic virtue. Once upon a time, the story goes, people lived within their means and borrowed only under the direst of circumstances. Debt was shameful, and credit financed only “productive” purchases like homes or farm machinery. But nostalgia seldom makes good history. Writers mourned this lost golden age during the Roaring Twenties, the rise of the credit card in the 1960s, and the home mortgage boom and bust of 2005–2008.

True, the instruments and institutions of twenty-first century credit—the installment plan, the credit card, and the home finance industry—are less than a century old. Yet credit itself is as old as commerce. “Buy Now, Pay Later: A History of Personal Credit,” draws on materials in Baker Library’s Historical Collections to show how previous generations devised creative ways of lending and borrowing long before credit cards.

The exhibit also shows how the credit industry evolved over time. Though credit is not new, it is newly visible. Personal borrowing—once private, often secretive, and sometimes even illegal—has become decidedly public: it is the business of major corporations and the subject of consumer protection regulation that seeks expand access to credit as well as to protect the borrower. Credit has moved from the fringes of the economy to its very center.1

1 Louis Hyman, “Debtor Nation: How Consumer Credit Built Postwar America,” Enterprise & Society 9, no. 4 (December 2008): 614–618.