“About everyone who lives in what he calls

his own house is in debt.” 20

&mdash Anonymous Boston leather cutter, 1870

{kind=link}

Well into the 20th century, professional advice-givers urged prospective home-buyers to save the entire purchase price before acquiring a home. In practice, however, most home-buyers and home-builders after the Civil War got themselves a mortgage—or three or four.

By the 1920s, economists were becoming aware of the growing role of mortgage finance in the American economy though they did not fully understand its implications. “What does it mean that the number of mortgages on homes is increasing?” wondered census analysts in 1923. “Does it mean growing wealth or growing poverty?” 21 The double-edged sword of mass indebtedness became clear in the Great Depression, when foreclosures on residential properties soared alongside farm foreclosures.

Scholars still know relatively little about the American real estate industry before World War II. The U.S. Commerce Department did not begin collecting data on house prices until 1963, and the decentralized nature of building and financing homes posed obstacles to private organizations who tried to do the same.

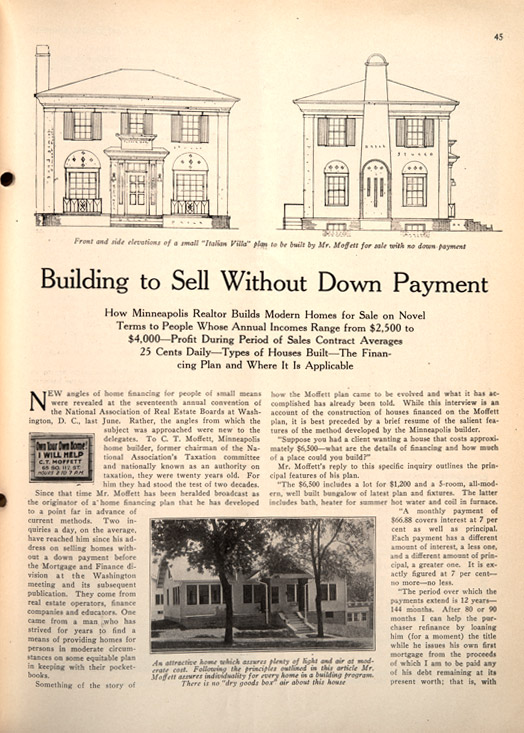

Anecdotal accounts, like this feature in the Ladies Home Journal in 1903, suggest that most home-buyers cobbled together financing from a variety of lenders for a single purchase. Government statistics identified friends and family, savings banks, and building & loan societies as the three largest sources of mortgage lending. Trade journals, like this report of too-easy financing during the real estate boom of the 1920s, offer the view from the industry’s side. 22

{kind=link}

{kind=link}

{kind=link}

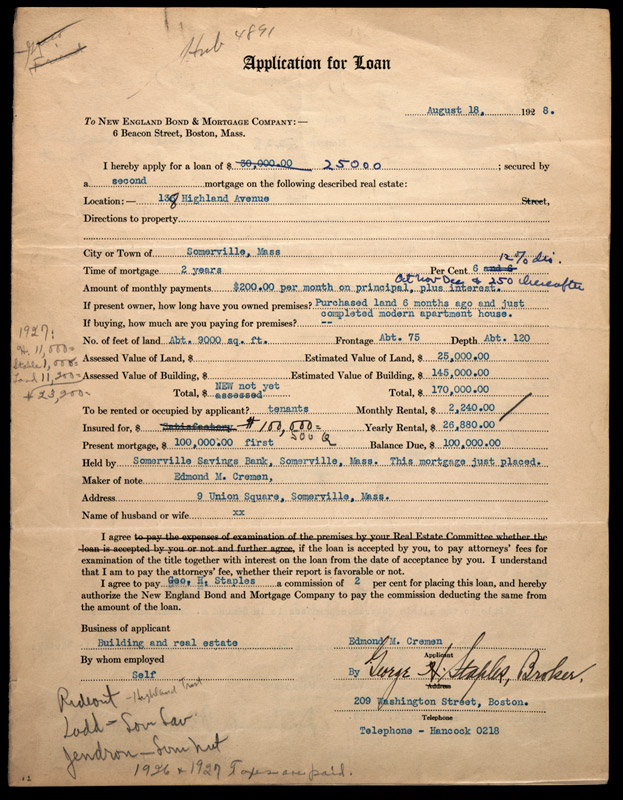

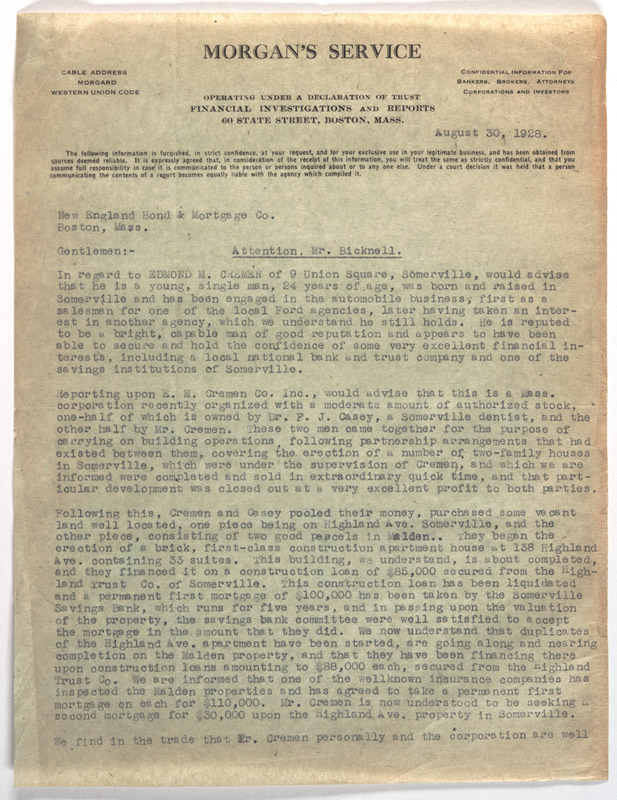

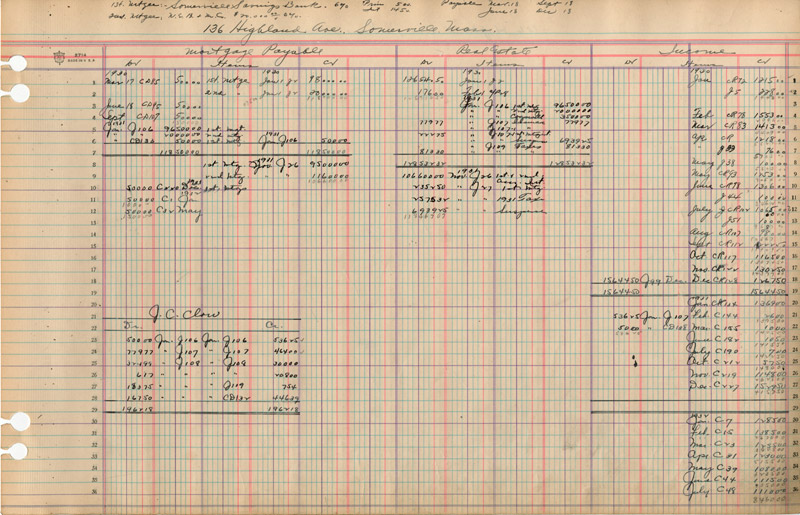

An unusual collection in Baker Library’s Historical Collections reveals a case study of Boston-area residential finance in the 1920s and 30s. In the early 1920s, Somerville entrepreneur Edmond M. Cremen moved into real estate finance from auto sales, another sector where credit was in the vanguard. The files of his financer, New England Bond & Mortgage, contain first, second, and third loans—none for a period longer than three years—on properties in Medford, Somerville, and Jamaica Plain. When the 1929 crash came, hoawever, it took Cremen down with it and the loan company was forced to foreclose on his mortgages. After managing the foreclosed properties for several years, New England Bond & Mortgage itself went into receivership in 1937.

20 Massachusetts Bureau of Labor Statistics, Report (1870), p. 188.

21 Thomas J. Fitzgerald and Richard Theodore Ely, Mortgages on Homes: A Report on the Results of the Inquiry as to the Mortgage Debt on Homes Other Than Farm Homes at the Fourteenth Census, 1920 (Washington: Govt. Print. Off, 1923), 12.

22 "Building to Sell Without Down Payment," National Real Estate Journal (Jan. 12, 1925), pp. 45-47.