Public pensions in the United States have sharply shifted their riskier investments from publicly traded stocks to alternative assets such as private equity and real estate over the past two decades.

While chronic underfunding in states and counties may seem like the obvious driver of this trend, a recent working paper points to a different story: some pension managers have simply become more bullish on alternatives relative to public equities. According to “The Rise of Alternatives,” these bullish beliefs are shaped by consultants, peers, and experience during the dot-com bubble in the early 2000s.

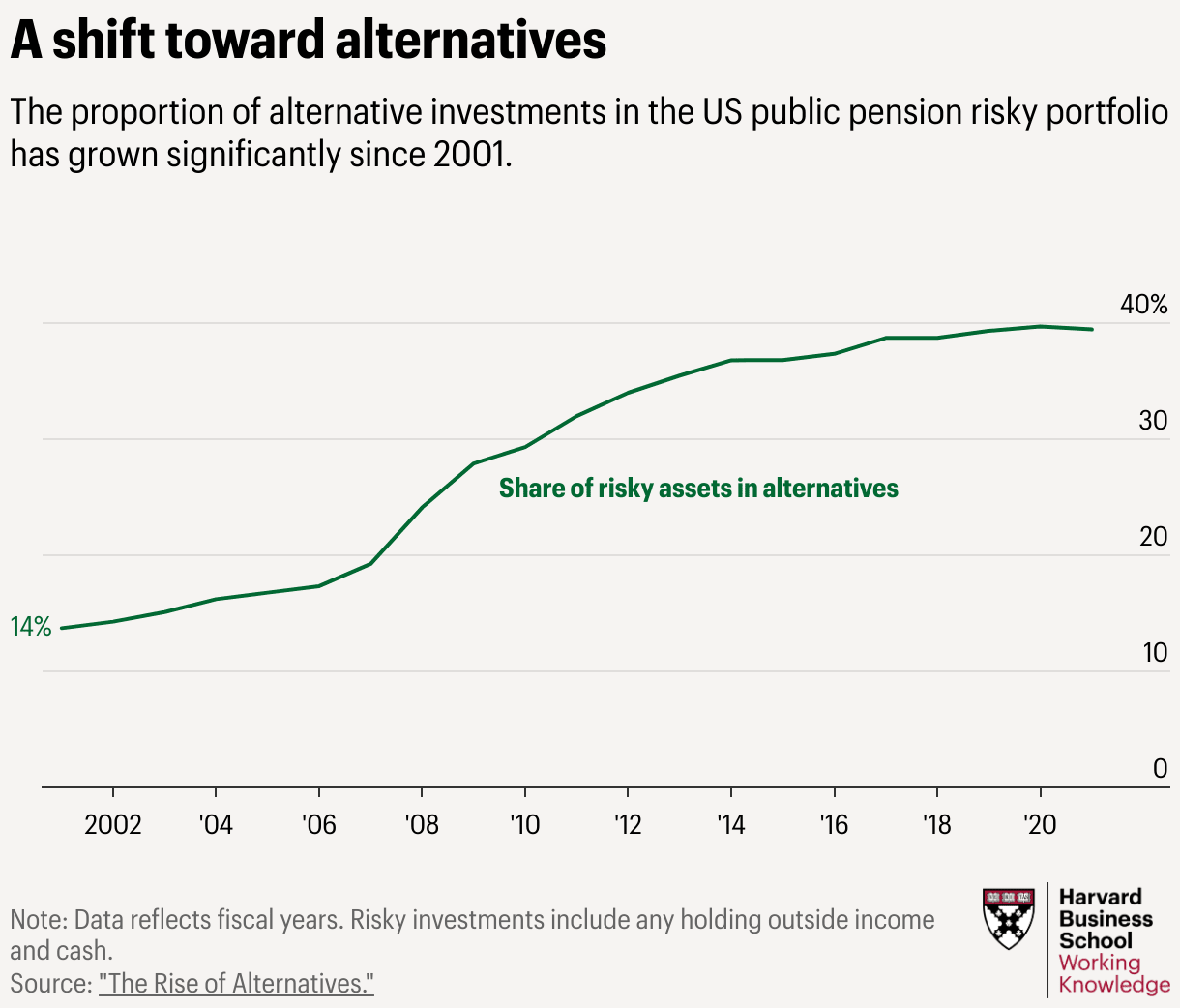

By 2021, alternative investments made up almost 40 percent of riskier allocations in public pension funds, up from 14 percent in 2001, says Emil Siriwardane, Harvard Business School’s Finnegan Family Associate Professor of Business Administration.

HBS Working Knowledge talked with Siriwardane to find out why state and local pension managers—who oversee roughly $6 trillion in retirement funds—are rethinking the riskier end of their portfolios. He conducted the research with Juliane Begenau, a professor at the Stanford Graduate School of Business, and Stanford doctoral student Pauline Liang.

The conversation has been lightly edited for length and clarity.

What surprised you about the shift to these riskier investments?

Emil Siriwardane: There was a narrative floating around when we started looking at the data several years ago, shortly after I joined HBS: interest rates have come down, public pensions are more underfunded, and they’ve turned to alternative investments to help close their funding gaps.

But it was surprisingly hard to find evidence for this narrative, as the most underfunded pensions have shifted just as aggressively toward alternatives as the best-funded ones. We then explored another hypothesis---one supported by textbook portfolio theory---that centered on beliefs: as interest rates came down, a lot of institutional investors, including public pensions, were probably encouraged to rethink their views on different asset classes and what's attractive and what's not attractive.

Our paper provides evidence that many pensions ultimately became more bullish on these alternative asset classes, like private equity, real estate private equity, and lately, private credit. They think it has a good risk-return profile, or a better risk-return profile, than they thought 20 years ago. And that seems to have driven a lot of capital flows.

What is the state of funding for pensions?

Siriwardane: With interest rates going up recently, it's gotten a little bit better. But US pensions are still about 60 to 70 percent underfunded. That is, for every $100 in pension liabilities, they have about $70 in assets to support it.

That’s at a national level, but there’s also lots of variation across states and counties. Wisconsin, for example, is a very well-funded state, whereas pensions in Illinois are among the most underfunded in the country.

How do you define alternatives?

Siriwardane: The definition of alternatives is ever-changing and will almost surely depend on who you ask. I think of alternatives as asset classes or investment products that are illiquid, opaque, and charge relatively high fees.

Right now, the biggest of those buckets is private equity, which is mature and fairly well-defined. Venture capital is a close cousin, and pensions often group it in with private equity when setting their asset allocation policies. Real estate private equity is another big bucket. It is structured a lot like private equity, but these funds buy properties, not companies. Private credit funds lend to companies versus buying them and is the fastest growing of this bunch. In all these asset classes, you give fund managers your money, you can't get it back for about 10 years, and you don’t always see exactly what they’re doing. This is quite different than, say, a mutual fund or an ETF.

Hedge funds are another type of alternative asset that is not always easy to define, but I think of them as traditionally investing in public markets, whereas all the other alternatives I mentioned transact in so-called private markets.

Are alternative investments less regulated than stocks?

Siriwardane: All of this is largely unregulated. That's another defining characteristic.

In another paper, we look at how pensions pay fees to these different [alternative] funds. It's quite opaque, so much so that pensions might pay different fees for the same exact investment product.

Under the Biden administration, the SEC had pushed for rules that would reduce opacity in private-market funds, but those efforts were dealt a serious legal blow last year, and it appears unlikely that the Trump administration will resurrect them.

Given that opacity, why are managers shifting?

Siriwardane: Pensions may be willing to accept the higher fees and opacity if they believe alternatives will deliver favorable risk-adjusted returns in the future. And historically, many of these alternative assets have delivered high returns relative to traditional asset classes like stocks and bonds, all while exhibiting a seemingly low correlation with these traditional investments.

The tricky thing is that alternative asset classes are very hard to benchmark, so it's possible for someone to think that they have lots of alpha—high returns relative to risk—whereas someone else might completely disagree. And neither can prove the other wrong. The scope for disagreement is high because the inherent illiquidity of alternative investments makes it difficult to measure their risk.

I think that's part of why you see such heterogeneity across pensions. Some have 70 percent of their risky assets in these alternatives. Other have none. It's quite drastic.

How were pensions influenced by the dot-com bubble?

Siriwardane: Well, for many public pensions, the 1990s was their first real foray in stocks. If you started investing in stocks earlier in the '90s, you had eight years of solid returns. And yes, the bursting of the dot-com bubble was unpleasant, but your first overall experience in the stock market was likely still positive.

But if you’re a pension that first invested meaningfully into stocks in 1996 or 1997, your experience was marked by high volatility and low returns. It was a unique moment for stock markets and one that likely tainted your view of public markets going forward. Our paper shows this mechanism can partly explain why some pensions came to prefer alternatives over public equities after the 2000s.

What conclusions can pensions draw from your research?

Siriwardane: The message of the paper is that beliefs are important for understanding why some pensions invest heavily in alternatives. This observation raises a practical question: how do pensions form beliefs? For instance, if you believe private equity will outperform public markets, let’s talk about why. How did you come to that conclusion? What data are you using? Have you been accurate in the past? Are your beliefs justified by the performance of your available investment managers? The point here is to have to an empirically grounded process by which your beliefs are formed.

My view is that with alternatives, like most forms of active investing, there's decreasing returns to scale when it comes to creating alpha. In other words, the bigger you get, the harder it is to outperform, in part because there's more competition. There's more eyes on each transaction.

The implication is that being early to the party in alternatives is advantageous, as it was for endowments in the 80s and 90s. But the landscape has significantly changed over the last thirty years. There’s a lot more competition, especially among the larger alternative asset managers with whom pensions tend to invest. So, my concern is that public pensions may have arrived at the party too late and are now paying fees in these asset classes that are not justified by their performance.

Image by HBS Working Knowledge with assets from BillionPhotos.com for AdobeStock.