Option Pricing in Theory & Practice: The Nobel Prize Research of Robert C. Merton

The Formula

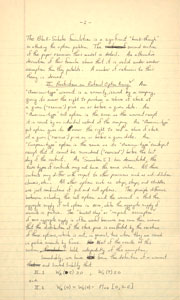

“Restrictions on Options Pricing” manuscript. Robert Cox Merton Papers, HBS Archives, Baker Library Historical Collections

In 1970, Robert Merton joined Myron Scholes at the Sloan School of Management, becoming the sixth member of the finance faculty. It was in this small group that the complex theories of option pricing and corporate liability valuation were developed and expanded upon. Though Fischer Black was not a member of the MIT faculty, he was a frequent visitor and valuable participant in the discussions held there. Over the next several years, these three economists both independently and collaboratively created option pricing theory. Early empirical tests of what became known as the Black-Scholes formula were published in 1972. The theoretical account finally appeared in 1973, after several attempts to find a journal willing to accept the article. Merton was closely involved in the work leading up to these publications and his own extensions of the formula appeared in print in the spring of 1973.