{kind=link}

{kind=link}

{kind=link}

As pioneers of the nascent information industry, the nineteenth-century credit ratings firms survived near-fatal attacks on several fronts. The Mercantile Agency was vulnerable to competitors who plagiarized their laboriously collected credit reports and distributed them under their own names. To foil this type of piracy, firm leaders asserted strong legal rights over the Agency’s data, and even included fictitious credit ratings in its books. Rivals duplicating this imaginary data in their own publications could be prosecuted, and at least a dozen rival firms came and went by the end of the century. Merchants themselves were more apt to sue if the Agency gave them advice about prospective trading partners that turned out to be wrong than if they learned they had received an unfavorable rating.

The case law and regulatory structure arising out of these legal challenges set precedents that continue to influence the law relating to privacy, libel, and intellectual property today.

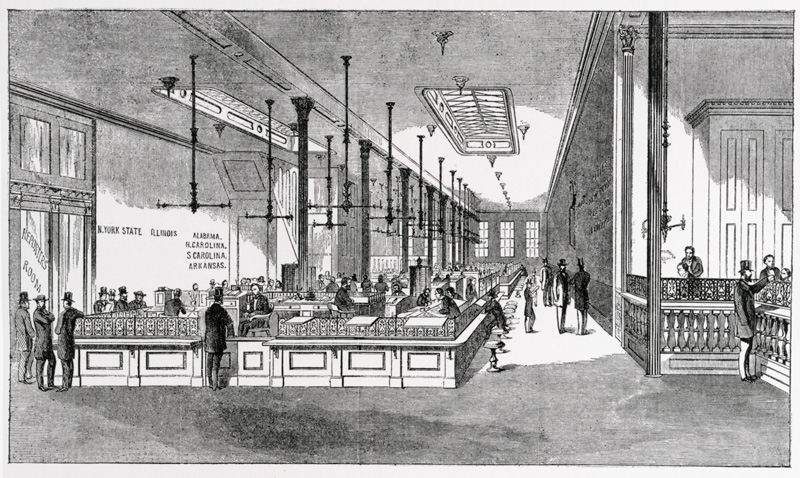

The nineteenth-century Mercantile Agency was a mix of old and new. Though Tappan and his successors heralded the coming information age in their dedication to the rapid collection, centralization, storage, and dissemination of data, the credit reports they gathered had little in common with the terse list of payment histories that appear in credit reports today.13

In addition to relatively objective assessments of wealth, the credit reports of the nineteenth century included subjective character assessments, often based on hearsay. Even the Agency’s guides to its own credit reporters admitted that the process was “unavoidably impressionistic.”14 Moreover, it was secret: an individual had no legal access to his or her own credit report. Under the circumstances, libel suits were inevitable. Early suits went against the firm, but by the end of the century a body of case law upheld the position that credit reports fell within the definition of “privileged communication” and thus were immune from the charge of libel.15 This decision secured the future of credit reporting.

13 Ingrid Jeacle and Eamonn J. Walsh, “From Moral Evaluation to Rationalization: Accounting and the Shifting Technologies of Credit,” Accounting, Organizations and Society 27, no. 8 (November 2002): 737–761.

14 Report Writers’ Guide (1918), p. 5. Dun & Bradstreet Corporation Records, Box 18, Folder 13.

15 James H. Madison, “The Evolution of Commercial Credit Reporting Agencies in Nineteenth-Century America,” The Business History Review 48, no. 2 (Summer 1974): 164–186.